not featured

2026-07-16

7/16/2026

Personal Banking

published

.jpg)

Financial Literacy Redefined: The Syllabus for Your 20s

Learning about the importance of saving and money management at an early age is crucial to building good financial habits that can help you achieve a more prosperous future and reach your goals. Most Americans wish they knew more about personal finance, which suggests they didn’t learn enough about it in school or from their families.

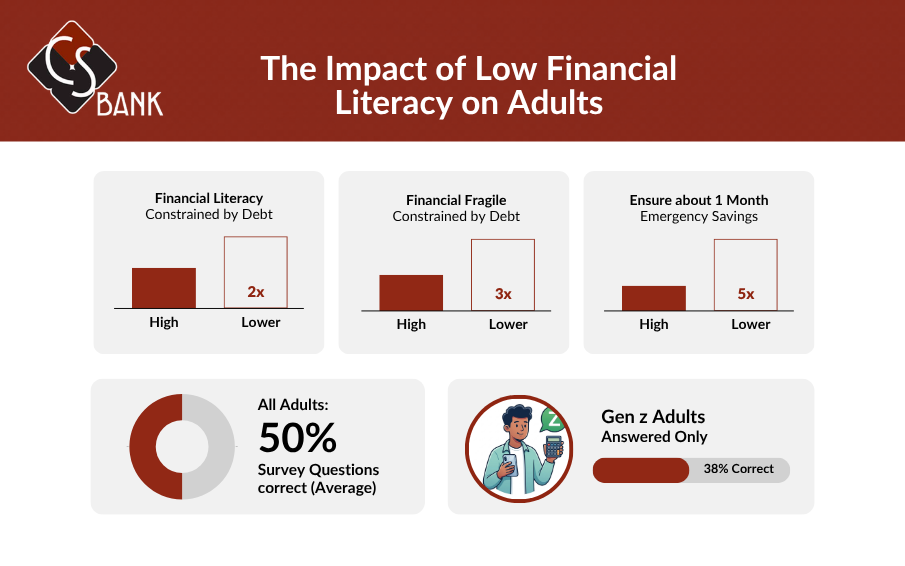

A study last year by the TIAA Institute found that adults with lower financial literacy are twice as likely to be constrained by debt, three times more likely to be financially fragile, and five times more likely to be unsure whether they have a month’s worth of emergency savings. Gen Z adults (those born between 1997 and 2012) answered just 38% of the survey questions correctly.

That’s why we put together these financial tips for young adults who may be wondering how to manage money in their 20s and beyond.

Course 1: Reading Your First Real Paycheck

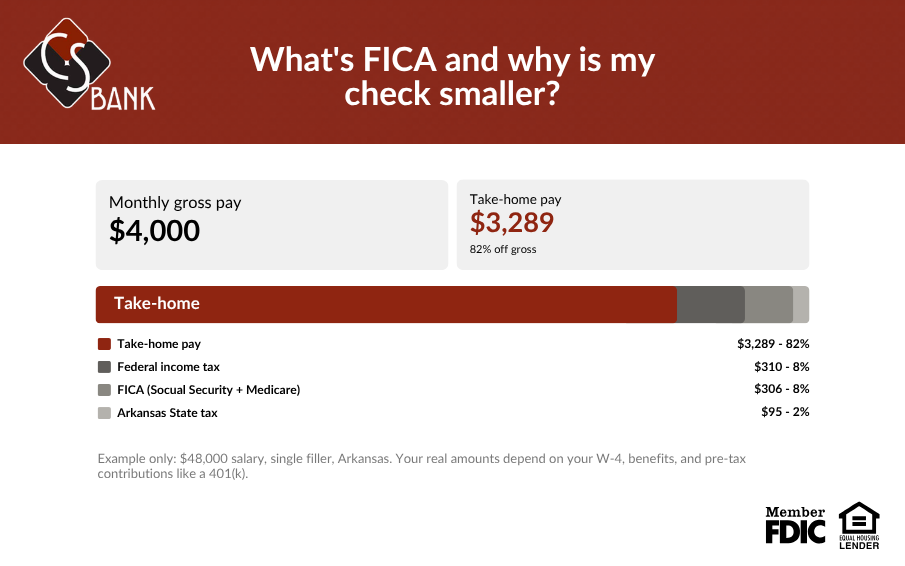

Many people have looked at their first paycheck and discovered that it’s for much less than they expected. They may be wondering what FICA is and why it’s taking a bite out of their income. Here are some key terms to understand about your pay:

- Gross pay: The total amount you earned before taxes and other deductions are made. If you’re an hourly worker, your paycheck will indicate the number of hours worked and your hourly rate. For salaried employees, your gross pay is your annual salary divided by the number of pay periods in a year.

- Net pay: Also known as “take-home pay” because it’s the amount you get to take home with you or have deposited into your bank account. It’s your gross pay, minus the deductions.

- FICA: Your deductions for Social Security and Medicare, which are required by federal law. Social Security takes 6.2% of your gross income, and Medicare gets 1.45%.

- State and local taxes: Arkansas has a graduated income tax that ranges from 0% for those making $5,599 per year or less, up to 3.9% for annual incomes of $94,701 or more. The state does not have local income taxes. Missouri also has a graduated income tax that starts at 0% for the first $1,348 of taxable income and rises to 4.7% for incomes of $9,436 or more. Local governments may have their own payroll taxes.

Other deductions could be made for your contributions to an employer's health, dental, vision, and retirement plans such as a 401(k). These deductions are made on a pre-tax basis, so your contributions to these plans reduce the amount you have to pay in taxes.

Your paystub will also include your year-to-date (YTD) totals for income, taxes, and deductions. Even if you’re just starting your career and pinching your pennies, the earlier you start contributing as much as possible to your retirement, the better off you’ll be in the long run.

Employee Versus Contractor

One important distinction that you need to be aware of is the difference between employees and independent contractors. An employee works for a business continuously under the direct control of a supervisor. The employer must make payroll deductions for income taxes and may provide health and retirement benefits. Employees receive a W-2 form that they use to file their tax returns.

With independent contractors, companies do not withhold their income so a contractor must handle payroll taxes on their own. They would receive a 1099 form, and it would not include any deductions. If you are an independent contractor, make sure you set aside enough money so you can pay your own income taxes and FICA contributions. You may need to make quarterly payments to your state and local tax authorities, or you could be hit with a penalty later on. An accountant or tax preparer could help you with this.

The IRS has more information on the difference between employees and independent contractors online.

Course 2: Banking That Works for You

The sooner you have a bank account, the better off you’ll be in the long run. Without a bank account, you’ll be hit with check-cashing, bill payment, and money transfer fees that eat into your income. It also means you can’t sign up for direct deposit of your paychecks, income tax refunds, and government benefits.

A bank account solves all of these problems, while also allowing you to earn interest on what you save and making it easier for you to establish credit so you can qualify for loans and credit cards. You can also trust that your money is in a safe place and is much more secure than keeping it in a mason jar or stuffed under a mattress.

Of course, not all bank accounts are alike, so it's important to choose the right checking and savings accounts early on, so you can avoid any fees that a bank might charge you.

That's why we offer four checking account options with a variety of benefits, starting with our Kasasa Cash Back checking account, which earns cash back on your debit card purchases and has no monthly fees when you sign up for free eStatements.

If you are between 14 and 28, the CS Bank NextGen Saver is built for exactly this stage. It pays a high rate, has no monthly fee with eStatements, and even rewards you for the everyday banking habits you are probably already doing. We also offer seven savings account options.

Every account comes with free digital banking tools, a debit card, a digital wallet app, and you can send money to friends and family using Zelle.

Course 3: Building Credit from Zero

Many people start building a credit score when they turn 18 and can have their own credit card. It may be a student credit card, or they have one in their own name as an authorized user on a parent’s account.

Prepaid Versus Secured Credit Cards

Those who are unable to qualify for a regular credit card, because they have a low credit score or a limited credit history, might obtain a secured credit card. It would require you to give the provider a security deposit, which would determine the card’s credit limit. Many secured credit cards require you to have a bank account, or you could make your security deposit using a money order or a prepaid credit card.

A prepaid credit card works similarly to a gift card. Whatever money you add to your card is the amount you can spend, although there could be activation fees, monthly fees, or fees each time you make a purchase. Apart from this, the biggest difference between secured credit cards and prepaid cards is that a secured credit card helps you establish a credit history, but a prepaid card does not.

How to Check Your Credit Score

You can check your credit score and credit history by getting a free credit report each week from AnnualCreditReport.com. It will include three reports from the nation’s three credit reporting bureaus: Equifax, Experian, and TransUnion. If you see any inaccuracies, such as an account you don’t recognize, contact the bureau that lists the information in its report and have it corrected. An account you don’t recognize could be a sign of identity theft, so checking your credit score at least once per year is a good idea to see how you’re doing and to protect your credit.

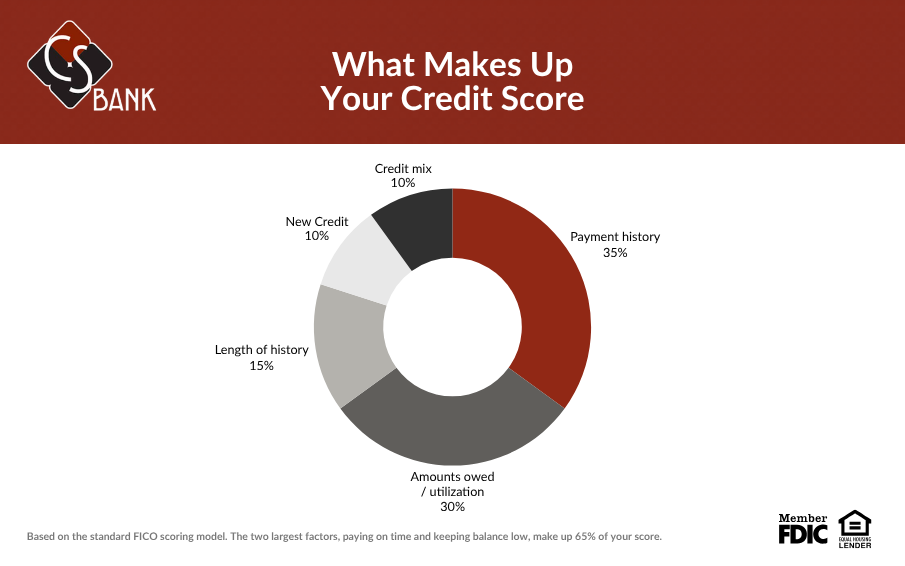

What Makes Up Your Credit Score

The three biggest components of your credit score are:

- Payment history and whether you pay your bills on time: 35%.

- Credit utilization, which is how much of your available credit you’re actually using across your credit cards and other loans: 30%.

- Your length of credit history. In other words, how long you’ve had each account: 15%.

The Importance of Having Good Credit

Whether you’re still in school or starting your career, having a good credit score is crucial. Many employers check your credit history as part of their screening process. A landlord might check your credit report before granting you a lease. A good credit score also helps you qualify for loans such as student loans, credit cards, auto loans, and mortgages. It also affects the interest rate you’ll have to pay. The higher your credit score, the better off you’ll be financially.

Many young people fall into a financial trap where they start living beyond their means and maxing out their credit cards. Whether it’s because your job just doesn’t pay enough for you to get by or your credit card makes it too easy to spend, the result is the same. It can hurt your credit score and hold you back financially and professionally.

How to Build and Maintain Good Credit

Paying all your bills on time is an important first step to building a good credit history, as well as keeping your debts as low as possible (including your credit card balance). Even if you obtain a new credit card with a higher limit, you should hold onto your older cards and use them once in a while to keep them active. Maintaining that pool of available credit helps your credit score in two ways. It keeps your credit utilization low (debts versus credit) and helps your length of credit history.

Course 4: The Savings Benchmark Question

If you’re considering how to build wealth in your 20s, we suggest you start by making a budget where you outline all of your income, your debts, and your monthly living costs. It should be as detailed as possible and include your financial goals and how you’ll reach them. You’ll need to go over this budget on a regular basis and keep track of all your spending.

If this seems like too much of a task, try doing it just for a month and see how it goes. At the end of the month, you can add up the totals and get a clear picture of how you spend your money, which can help you find ways of saving more, spending less, and reducing your debts. One of your first financial goals should be to establish an emergency fund, which is typically two to three months’ worth of your household living expenses. We suggest keeping it in a savings account, where you can earn interest.

Our younger customers frequently ask us: “How much money should I have saved by age 30 and beyond?” Financial experts recommend you have saved this much based on your age, which could be a combination of savings, investments, and a retirement plan:

- By age 30: One year’s worth of your income in savings.

- By age 40: Three times your annual income in savings.

- By age 50: Six times your annual income in savings.

- By age 60: Up to eight times your annual income in savings.

If this seems like an impossible task, try building an emergency fund first, followed by your other financial goals. We offer additional information on this subject in our post: 7 Habits to Help You Build Wealth.

Course 5: Investing Early Is the Cheat Code

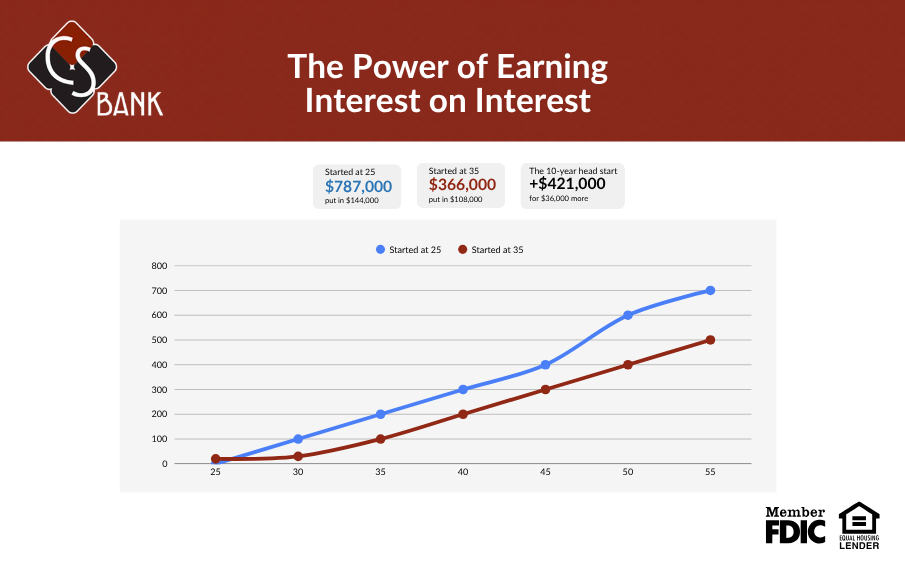

While there isn’t any fast and easy way to build wealth, one of the best approaches is to save as much as you can as early as possible so you can make the most of compound interest, which is also known as “earning interest on interest.” As your savings and investments accumulate, each year you’ll earn interest on what you set aside (the principal). You’ll also earn interest on your previous earnings. That’s why saving early and as much as possible is so important. If your employer offers a retirement plan, try to contribute as much as possible. If they match your contributions, you should at least invest the amount necessary to maximize this benefit. Not only are your 401(k) contributions tax-deferred, but any matching funds your employer offers are like earning free money.

Open an Account or Speak with a Banker Today

Ready to get started? You can open an account online in just a few minutes, or stop by your local CS Bank in Harrison, Berryville, Eureka Springs, Huntsville, AR, or Cassville, MO, if you'd rather talk it through with someone.